What’s going on at Silicon Valley Bank?!

Quick overview of the SVB situation unfolding

After the Wednesday announcement by SVB (raising capital) and Thursday’s fall in SVB’s share price (~60%, $SIVB), all I’m hearing about are startups concerned with the safety of their money at SVB. It’s especially interesting given SVB is seen as a safe haven in Silicon Valley, so many tech startups hold a lot of their cash there without much thought to it.

I’ve put together some quick context on the situation. Will definitely be interesting to follow in the coming days/weeks, hopefully SVB can find a path forward and customers are unharmed. Note the below numbers are all on-balance sheet and are for illustrative purposes only.

Just starting out writing, like or subscribe to let me know you’d like to hear more.

Edits: Actual post starts further below

This is unfolding faster than expected, SVB is trying to sell itself

SVB has been shut down by regulators and FDIC is stepping in

FDIC is moving fast, they’ve set up a new bank and transferred insured deposits, uninsured deposits will receive receivership certificates (illiquid, timing uncertain)

This is going to have a profound impact on startups that banked there (hearing 93%+ of SVB deposits exceeded FDIC insurance limits), hopefully they can find a way to make payroll so employees aren’t hurt

SVB support group chat, lots of useful information

Part 2 with more detail and what to watch going forward

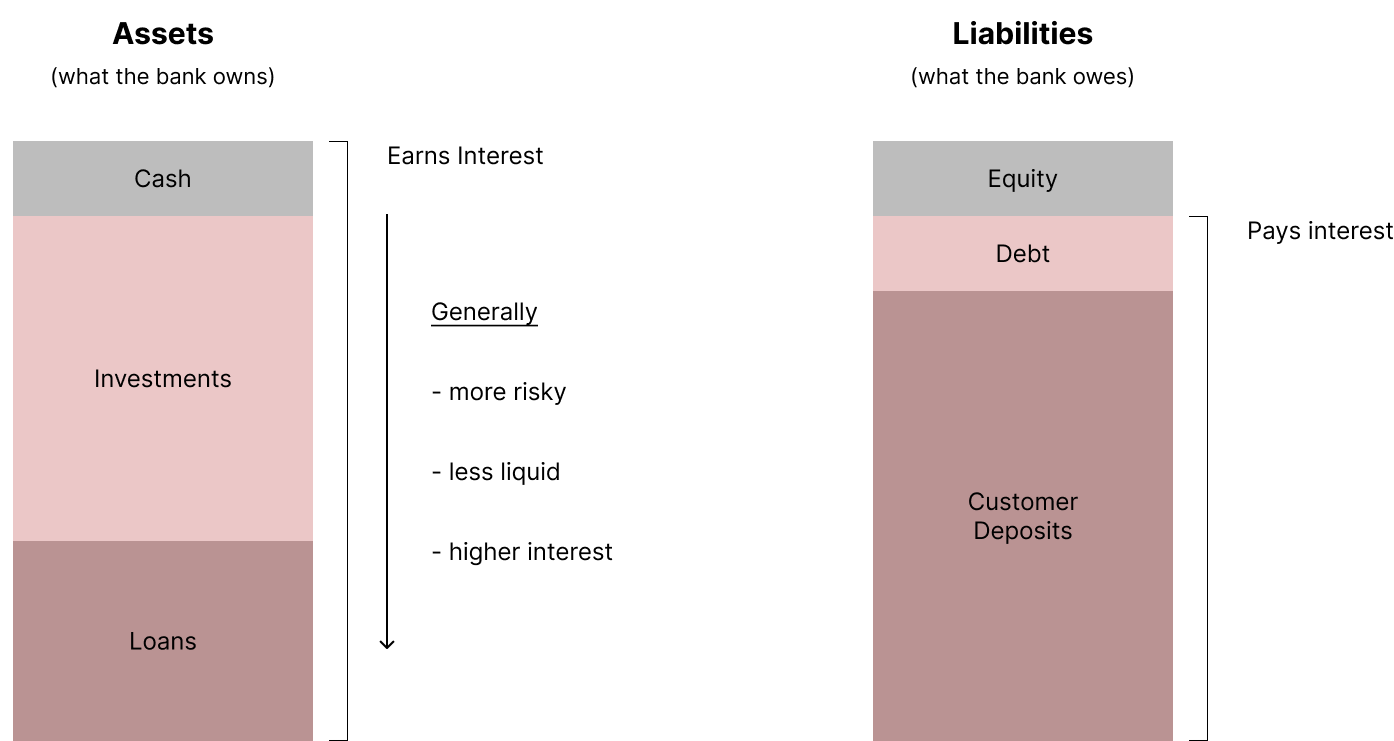

TLDR - How Banks Work

Banks raise money from customers deposits, debt, and equity

Hold the money in cash, investments, or give it out as loans

Profit (net interest margin) = interest earned - interest paid

Banks have strong incentives to put more money in risky loans that pay higher interest rates to boost profits

Restricted by regulations on how much they can put in loans and investments to customer deposits and make sure consumers can get their money

Situation at SVB before announcement

SVB’s deposits surged through 2021, primarily from startups and tech companies

Those companies continue to burn a lot of cash but are no longer raising vast amounts of money given the VC funding market has frozen up

Resulting in decreases in deposits (funds being withdrawn from the bank)

SVB deposits peaked in Q1-2022 and have been declining since

The bank only holds a small amount of cash (normal), if withdrawals are large enough it has to tap its other assets (investments and loans)

SVB Announcement

The company announced two key things on Wednesday:

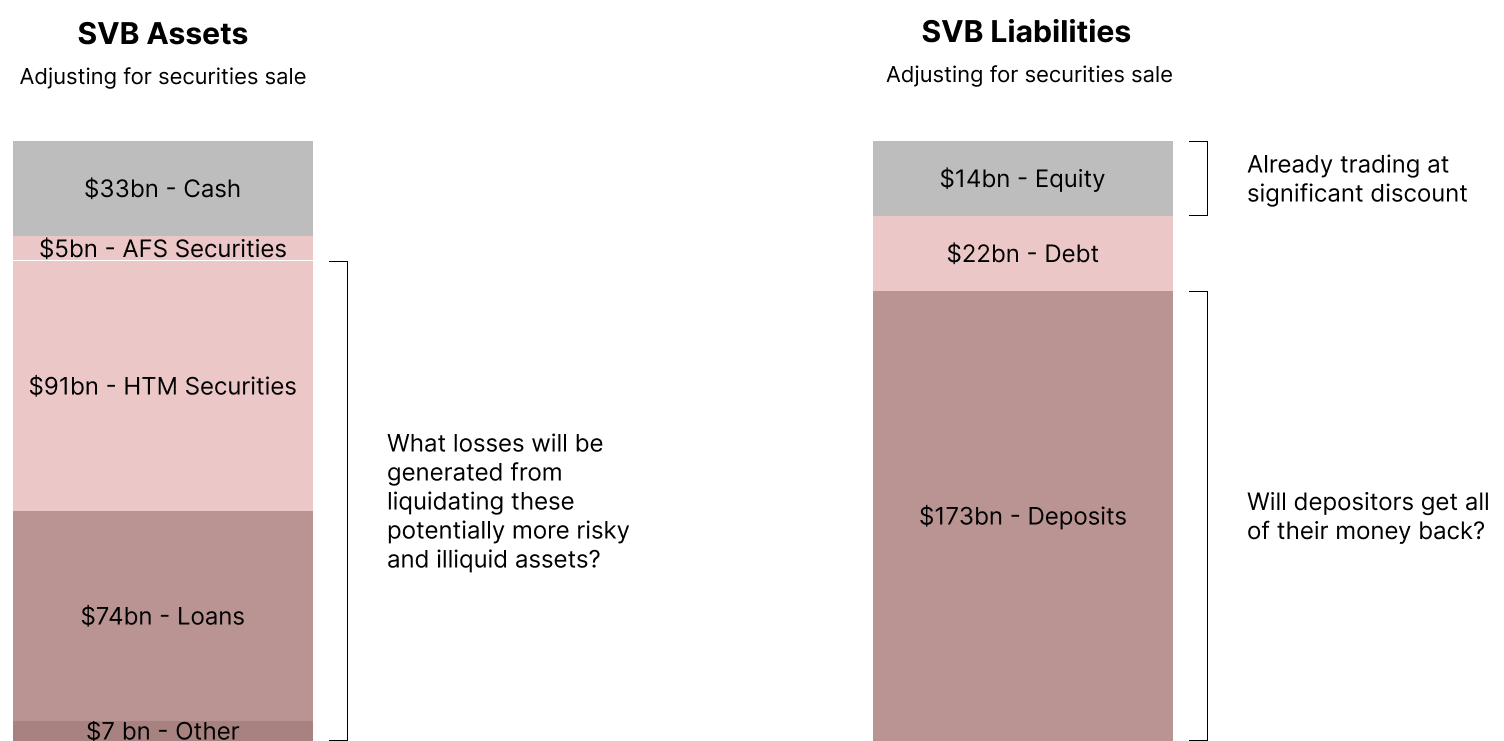

In order have enough cash to manage potential withdrawals, SVB sold a large amount of its investments ($21 billion of AFS Securities) and took a $1.8 billion loss (~10%), only received $19 billion of cash

They are attempting to raise $2.25 billion of fresh equity capital, to further make sure they have enough cash

Part of the capital raise is coming from a very well known and respected investor (General Atlantic)

The bank adjusted for the announcement

While these two actions are helpful in building up cash to manage withdrawals, it’s also created a panic in two places:

Share price has fallen dramatically (~60% in one day), so shareholders are significantly less optimistic about the future of the company

Tech startups/companies that hold all their money at SVB without much thought, are for the first time seriously concerned about the safety of that money

Reportedly Founder’s Fund has advised their portfolio companies to move cash to another bank

From conversations I’ve been hearing and on Twitter, seems like lots of companies are thinking the same thing

SVB has a very concentrated customer base (tech companies and VC) so this could move quite quickly

It’s all a confidence game at this point

Going forward?

It seems like all the cash raised by SVB was for normal business, to manage withdrawals due to continuing cash burn at startups. If this new frenzy causes mass withdrawals, it’s unclear if the cash is enough to manage that additional pressure. Mass withdrawals tend to be very self-reinforcing because no one wants to be left holding the bag (bank run), especially when things can go viral so fast. Will this be the first mass viral bank run?

If things head down this path, a couple key concerns come into focus:

To manage excessive withdrawals, will SVB have to sell additional assets (Investments and Loans) to come up with the cash?

They already started with $21 billion of AFS securities which sold for a ~10% discount, a $1.8 billion loss

The AFS securities might have been the best assets, what does this imply for the HTM Securities and Loans?

Will HTM Securities and Loans go for higher discounts and create significantly larger losses?

The current rising rate environment is making it tough to sell these assets

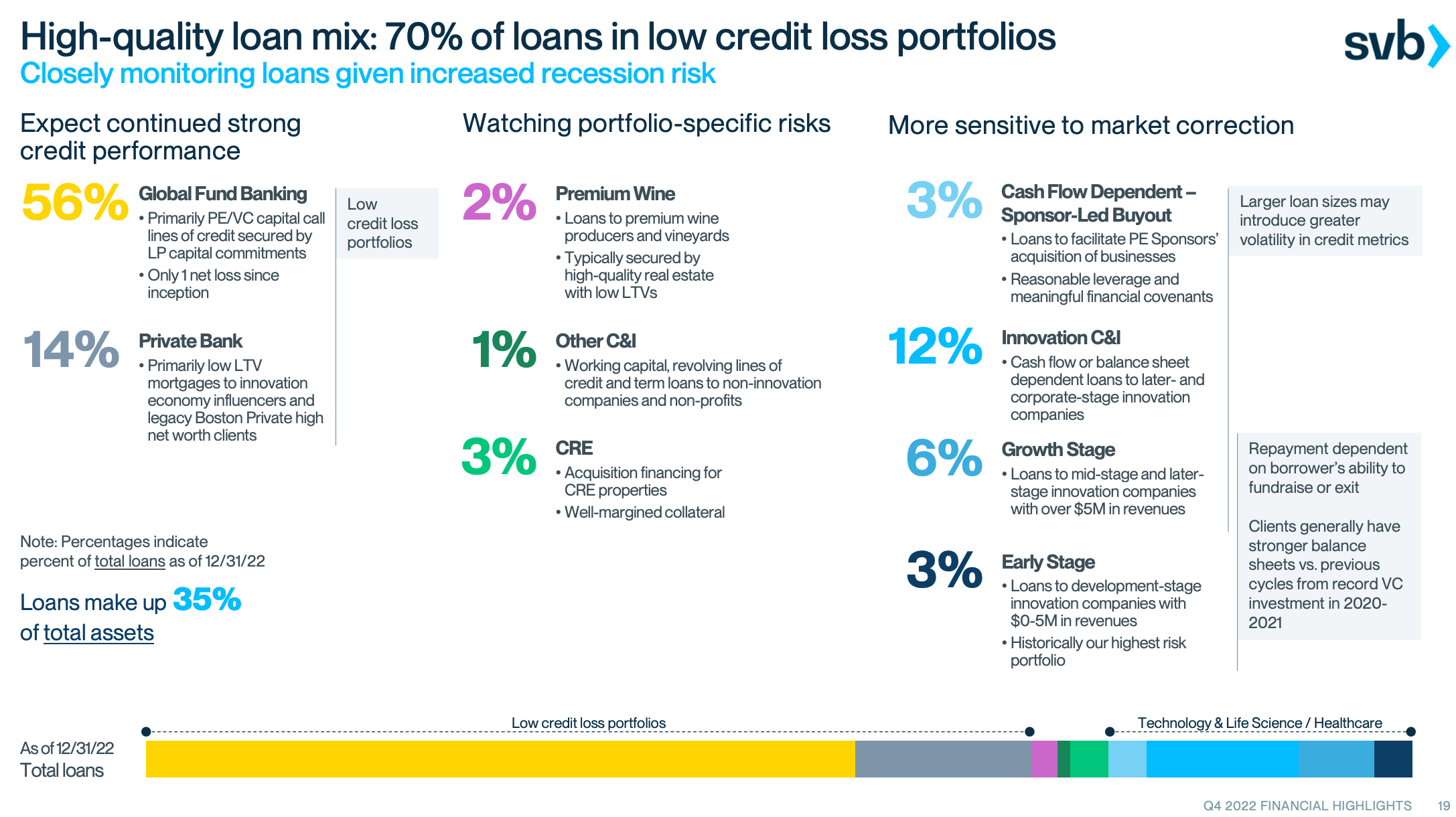

I expect financial analysts with a lot more experience will be opining on the loan book soon, see below for detail provided by SVB

Will customers end up getting hurt because they can’t withdraw their deposits?

How will this impact the tech industry given SVB’s prominent role?

Is this a broader problem here?

Will the government have to step in?

Hope this was helpful. Subscribe for more or follow me on twitter @manubhat_

SVB Loan Book Detail

SVB Info

Disclaimer

Information in this post should not be considered investment advice or fully accurate.

Thank you Anshuman!