SVB demise + what’s next?

Quick overview of what's happened and where things are headed

Only when the tide goes out do you discover who's been swimming naked. - Warren Buffett

First and foremost, my thoughts go out to all the founders and employees of companies that had significant funds at SVB or other potentially affected banks. Hopefully one of the solutions below plays out and companies can meet their payroll 🙏

Edit:

Reports of the government working on an additional backstop facility to calm contagion fears

Government has been running a sales process for SVB with the goal of finding a buyer this weekend

Details of the government backstop coming out, looking like depositors will be fully protected 💯🙌

Regional bank stocks (e.g. First Republic Bank) are still being affected. While the gov’t backstop helps depositors and reduces bank run risk, it specifically doesn’t help shareholders. As I mentioned below, focus is shifting to unrealized losses on loans and investments on bank balance sheets

Recap

Wed - SVB announced they had to sell assets and will raise capital to increase cash levels, spurred by a potential Moody’s downgrade

Thur - Massive drop in SVB stock alerts tech world that their SVB deposits may be in jeopardy. Frenzy ensues and $40+ billion withdrawn from SVB in 24 hours, ~25% of total deposits

Fri - FDIC takes over and closes SVB, insured deposits (up to $250k per customer) are transferred to a fresh bank opening on Monday, uninsured deposits (90%+ of all SVB deposits) are given certificates. Minimal information on ultimate recovery of those certificates or timeline. Companies with funds at SVB are scrambling

Sat/Sun - Calls for and against gov’t bailouts, concerns of systemic risk (regional banking crisis), gov’t and private sector working overtime for a path forward

Mon - ??

SVB - perfect storm or obvious oversight?

An argument can be made that this was a perfect storm:

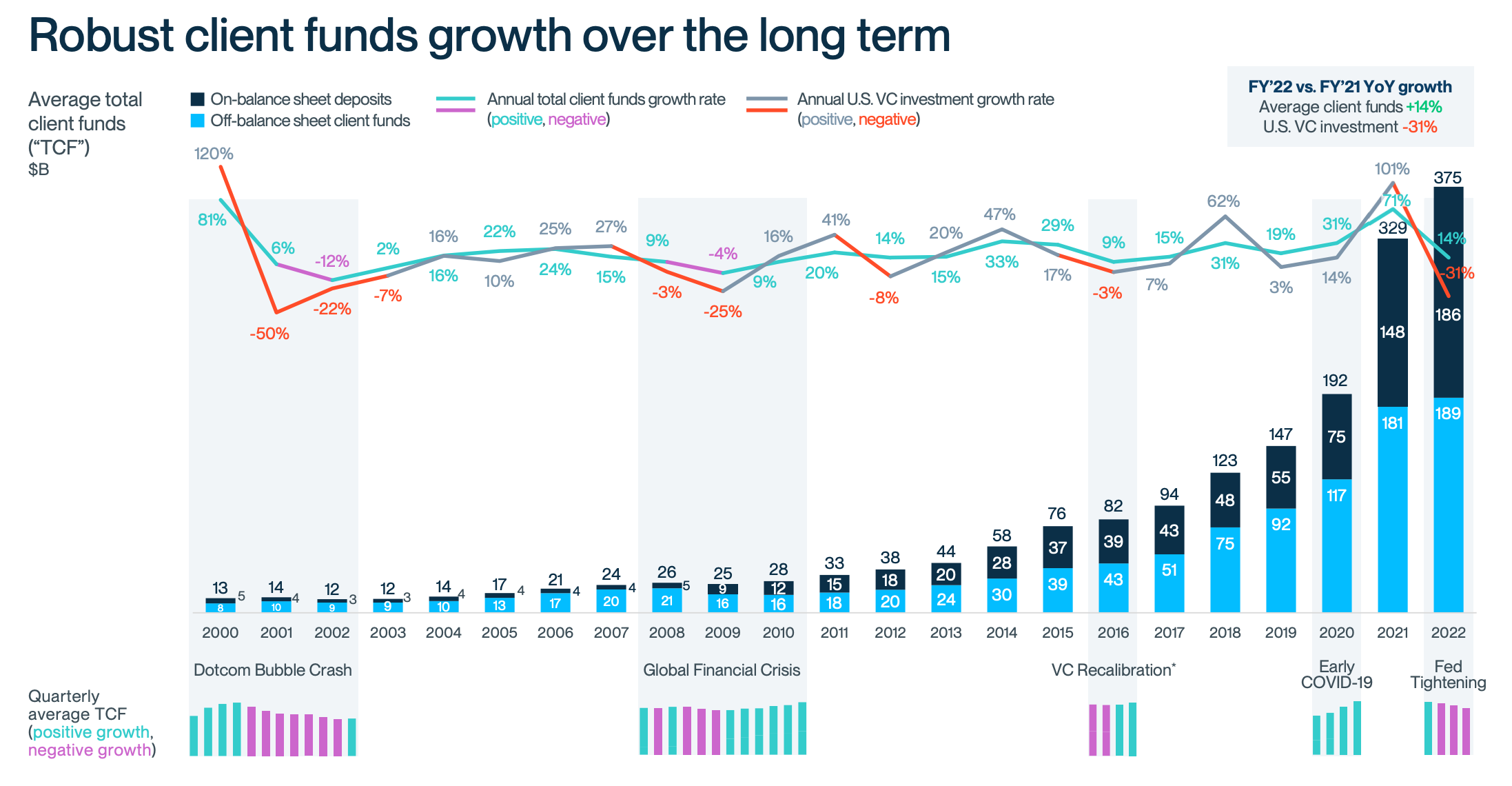

20’-22’ VC/tech froth flowed to SVB and deposits grew from $55 billion in 2019 to $191 billion in Q1 2022, 3.5x in just 2 years

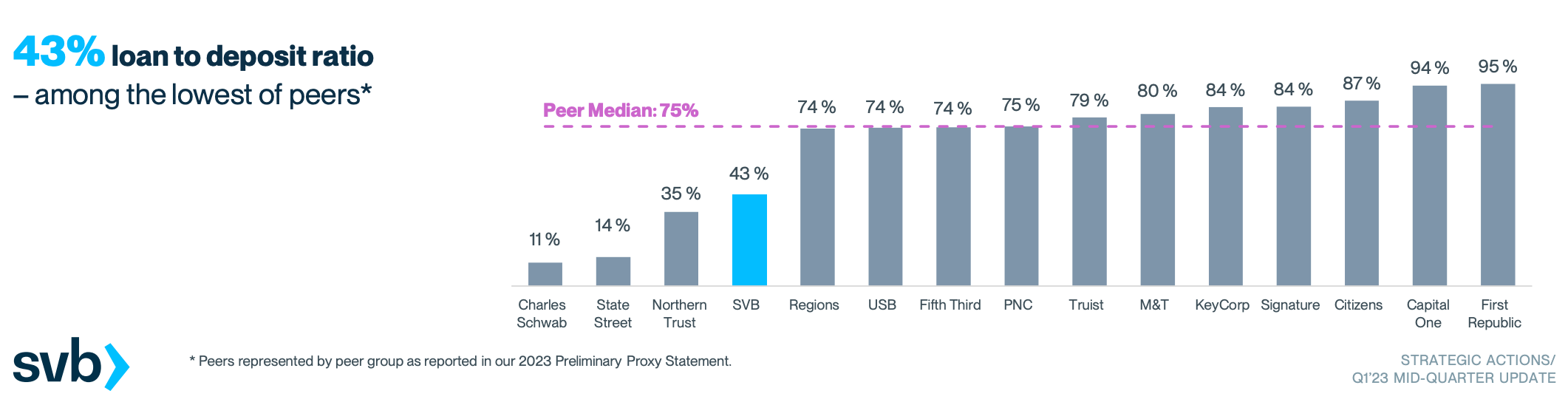

SVB invested those deposits into investments/loans and was actually quite conservative relative to most banks. Their loan-to-deposit ratio (amount they invested into riskier and more illiquid loans) was quite low, but they had to invest (80%+) at the absolute worst time, when the fed had rates set near zero

Right after deposits peaked in Q1 22, the Fed starts raising rates significantly to fight inflation. This causes the value of even the safer investments to drop significantly.

For normal course of business, SVB sells some of those safer investments at a ~10% loss. This spooks stockholders which spooks customers and the rest is history

To be clear, almost no bank can manage 25% of deposits being withdrawn in one day

Was this an obvious oversight?

Hindsight is 20/20 and everyone is piling onto SVB, but they basically had to invest as they receive deposits, otherwise stockholders would have fired management at the time, and they did so decently conservatively (relatively…)

Where did they mess up?

While they did a good job (relative to other banks) of not investing too aggressively in riskier/illiquid loans and focused on higher quality investments, they royally f*d up with duration

SVB invested heavily into safe but long dated 10+ year investments instead of safe 3 month - 1 year investments. This was profit motivated since the fed keeping rates near zero (at the time) meant those shorter duration investments barely yielded anything (~0.5% interest), while they made ~3% interest on the 10 year investments

The importance of this duration issue is that in the event you need to sell your long dated investments and rates significantly rise (which they did), the going price for these investments (even though they are safe) drops significantly

SVB would not have had this issue if they had instead invested in shorter dated securities (sacrificing short-term profits) or put proper interest rate hedges in place

SVB underestimated the possibility of rates rising quickly

While we all knew it was coming, it was extremely hard to have known just how fast it would come. That said, its the job of risk control teams at banks to prepare for those tail risks (unclear if this was even a true tail risk)

SVB overestimated the stability of their deposits

Their customer base was unique and they should have been even more conservative

Customers are primarily tech companies with very high cash burns, meaning their deposits were bound to rapidly decline

Second, their customer base is extremely concentrated with just tech companies and VC firms, making their risk of a bank run extremely high

Mistakes were clearly made. While it looks like just SVB right now, I’d bet we’re going to see more poor decision making revealed across the industry, hopefully not to the same extent…

SVB - What now?

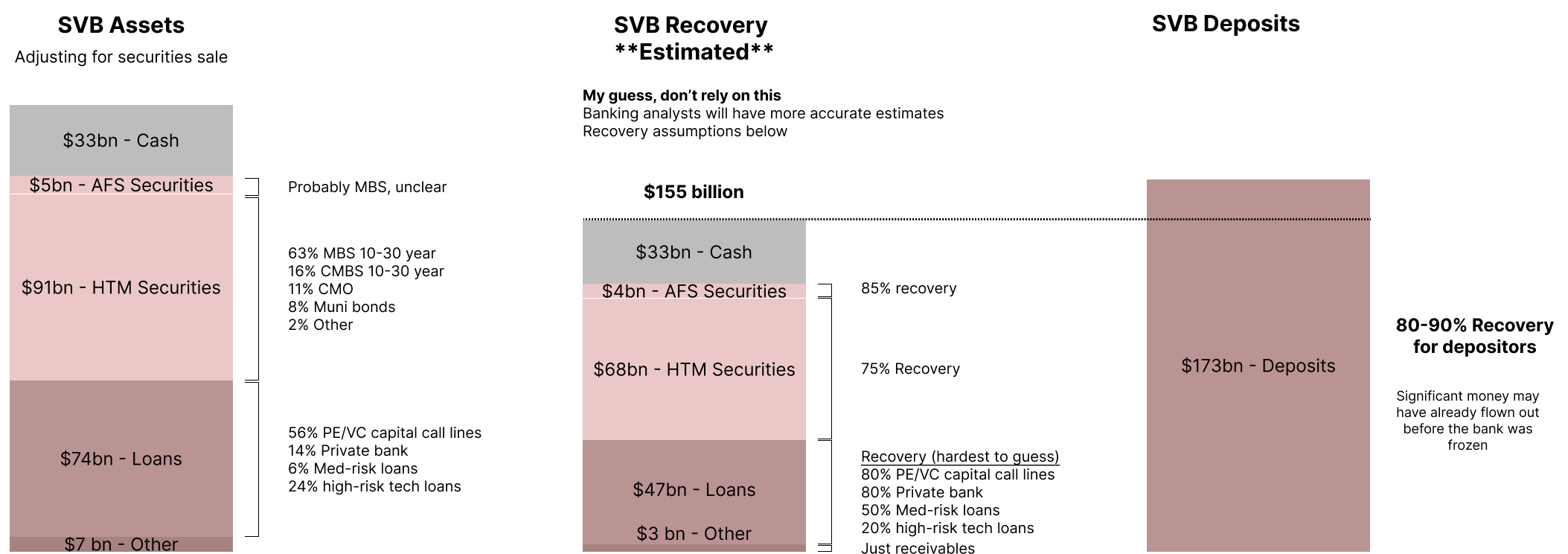

Insured deposits (up to $250k) should be available via the FDIC’s new bank on Monday. However 90%+ of deposits were uninsured and received certificates which effectively made them creditors in the bankruptcy of SVB. While those certificates will probably receive most of their money, it’s very unclear when and companies can’t make payroll with just $250k.

A quick recovery analysis (above) makes me think customers will eventually receive 80-90% of the value of their certificates.

Founders are reporting various hedge funds offering to buy their certificates for 60-70% of face value. Makes sense given funds are probably doing similar math as above and pricing in a 20% return

While this gives companies a quick path to more liquidity, they would be giving up 30-40% of the potential value of their cash deposits

The other private markets alternative is a larger and trusted bank/entity (e.g. Chase or Buffett) stepping in, guaranteeing all of the deposits, and taking over the bank

This would surprise me since they would be taking on quite a large potential loss without much upside (assuming no gov’t guarantee). Although I’m hearing there is some type of sales process being run by the government

Potential Solution

An accelerated ~50% partial payment from the gov’t to certificate holders early next week to help them avoid payroll/operational issues.

Between the cash and securities held at SVB, there is between 60-75% of the value of deposits that can be very quickly confirmed and liquidated

The government should be immediately selling those securities and paying out depositors, or provide an advanced payment of ~50%, an amount they can be highly confident they will recover from the cash and securities

Companies get immediate cash to continue payroll/operations and taxpayers take on minimal risk and won’t be bailing out the tech sector

The remainder of the deposits, primarily value from the loan portfolio, can be sorted out over a longer time

What’s next?

After SVB’s quick demise, the big question is will this bank run trigger a larger event? Is SVB a canary in the coal mine or just a unique situation? While I hope its the latter, here are a few points I believe will come into focus:

The real value of long-dated loan portfolios and HTM securities on bank balance sheets which are no longer accurate after rates have risen quickly. This will identify other banks that haven’t been prudent with risk. I would start with banks that also came into a lot of money over the past couple years

There are tighter regulations for banks over $250 billion (SVB was just under) which in theory would catch a lot of the issues here. So this may be more of a small bank (<$250 billion) problem (e.g. regional banks)

The increased risk of bank runs given they can happen much faster with the virality of the internet

The need for some sort of additional assurance by the government regarding deposits as the 250k FDIC insurance might not be enough anymore. There is already talk of the FDIC/Fed creating a special fund to further backstop deposits

It’s all about confidence at this point

Thanks for reading! If you found this helpful and think I should write more, please like/subscribe/share to let me know. You can follow me on twitter @manubhat_

Disclaimer: This post is not investment advice and is for information purposes only.